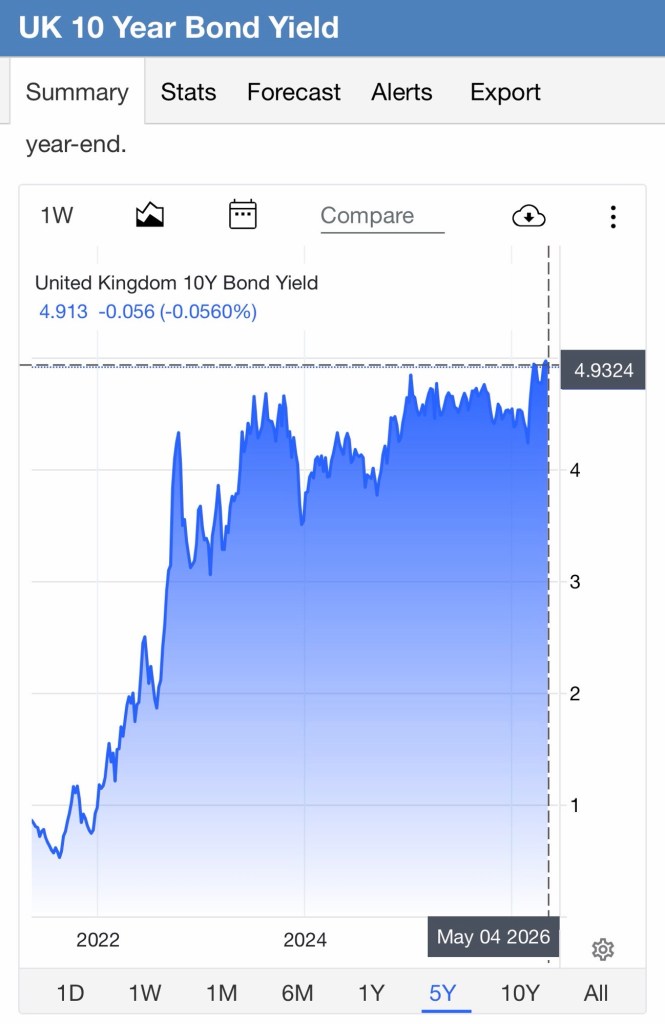

Britain has spent around 90% of Labour’s time in office borrowing at rates above the average level seen during the market turmoil of October 2022, despite inflation being far lower.

Labour came to office promising competence, stability and economic credibility. After fourteen years in opposition, they assured the country they had a plan for growth, investment and sound public finances.

It is therefore entirely reasonable to ask a simple question. If Labour has restored confidence in Britain’s economy, why are we still paying crisis-level borrowing costs?

That is not political spin. It is what the numbers tell us.

When Labour entered office in July 2024, the UK 10-year gilt yield, effectively the interest rate the Government pays to borrow money over a decade, stood at around 4.14%. Since then, Britain has spent around 90% of Labour’s time in office borrowing at rates above the average level seen during the market turmoil of October 2022.

If that mattered then, it should matter now.

The recent move back above 5% matters because it confirms this is no temporary wobble. Britain has quietly spent most of Labour’s time in office borrowing at rates associated with what politicians once described as an economic emergency.

Why should anybody care?

Because Britain does not borrow small amounts of money. The Government refinances hundreds of billions of pounds of debt every year while also borrowing to fund day-to-day spending. When borrowing becomes more expensive, taxpayers eventually pay the difference.

And Britain is paying more than many comparable countries.

Germany borrows for ten years at around 3%. France pays around 3.7%. Even the United States, despite its vast debt burden, has recently borrowed more cheaply than Britain at around 4.3% to 4.4%.

Britain recently moved back above 5%.

Of course, borrowing costs have risen across much of the developed world. Inflation, geopolitical instability and larger government borrowing have pushed rates higher internationally. But Britain is still paying a premium. Investors are demanding more to lend to us than many of our peers.

Before anyone reaches for the familiar claim that Labour inherited a mess, let us be honest about where the country stood in mid-2024.

Britain still carried substantial debt after COVID, which Labour and Liberal Democrats wanted to expand further and for longer. Families had been hit hard by inflation and soaring energy costs following Russia’s invasion of Ukraine. Nobody sensible would pretend the economy was in perfect condition.

But neither was Britain in freefall.

By July 2024, much of the hardest work had already been done. Inflation had fallen sharply from its peak. Energy prices had eased. Financial markets had stabilised. Interest rates had likely peaked and wages were beginning to recover in real terms. Growth remained weak, certainly, but the economy had steadied.

Labour then made choices. Bad ones.

At precisely the moment Britain needed stronger growth and business confidence, ministers chose higher taxes, higher employment costs and higher spending.

The rise in employer National Insurance alone is expected to raise around £24.5 billion a year for the Treasury. Ministers describe that as a tax on business , not workers. In reality, businesses do not absorb costs by magic. When employing people becomes more expensive, recruitment slows, investment is delayed and costs are passed on.

Sometimes jobs simply never appear.

We are already seeing warning signs. Unemployment has risen to 4.9%. The number of people on payrolls has fallen. Business insolvencies remain elevated.

No credible person would claim Labour caused every business failure or every economic problem. But it is entirely reasonable to ask whether this was really the moment to make employing people more expensive.

The same concern applies to farming.

Agriculture was already under pressure from volatile prices, changing subsidy arrangements and rising costs. Yet Labour chose to add more uncertainty through changes to inheritance tax reliefs affecting farms and family businesses.

For many farming families, this is not an abstract policy debate. It is about whether a viable family farm survives to the next generation. Food security matters. Domestic production matters. Confidence matters.

Then there is public spending.

Nobody disputes that doctors, nurses and public sector workers deserve fair pay. But taxpayers are entitled to ask what they receive in return. Where was the transformation package? Where was the productivity deal? Where were the measurable improvements in outcomes or efficiency?

Pay has increased. Yet many public services remain under pressure.

The deeper concern is philosophical.

This Government too often appears to see enterprise first as a source of revenue rather than the engine of growth. Economies grow when people are prepared to take risks, invest, employ others and build businesses.

Too few around the Cabinet table seem to understand what it takes to build a business, meet payroll and employ people when margins are tight. Those decisions carry risk. Ministers should remember that before making growth harder.

Yet too often, the instinct feels like the same old Labour answer. More tax. More regulation. More spending.

The cost of these choices lands directly on the public finances.

Britain is expected to spend around £111 billion this year simply paying interest on debt. That is more than £300 million every single day, or around £3,900 for every household in the country.

Britain’s debt is now so large that even small rises in borrowing costs make a big difference.

As a rough guide, every 0.1 percentage point increase in long-term borrowing costs adds around £1 billion a year to what the country eventually pays. A rise of half a percent could add around £5 billion. The Office for Budget Responsibility estimates that a sustained one percentage point rise could add between £10 billion and £15 billion a year to debt interest costs.

That is money the country no longer has for other priorities.

Money that could strengthen defence, improve roads, invest in technical skills, modernise infrastructure or ease pressure on taxpayers.

Instead, it goes on servicing debt.

And defence matters.

Defence spending is not simply cost. It creates skilled jobs, supports manufacturing and drives innovation. It strengthens supply chains, boosts exports and helps make Britain safer in a more dangerous world.

Yet Britain is increasingly spending vast sums paying interest rather than investing in national resilience. That is the real cost of weak public finances.

Britain already carries close to £3 trillion of debt. Small movements in borrowing costs now carry very large consequences. Higher borrowing costs leave less room to strengthen defence, less for policing, less for roads and local services, and less flexibility elsewhere in the public finances.

Governments eventually have only three choices. Borrow more. Tax more. Or spend less.

There is no escaping the arithmetic.

Labour says it has restored stability. Yet investors appear less convinced. They look at growth, debt, spending and risk. Right now, Britain continues to borrow at rates associated with a period politicians once described as an economic emergency.

After fourteen years preparing for government, Labour cannot blame inheritance forever. These are now their decisions, their priorities and their consequences.

Britain is stronger than sudden collapse. The greater risk is slower but sustained decline. Weak growth. Higher taxes. Rising dependency. More debt and less competitiveness while ministers convince themselves that managing decline is the same thing as governing.

Voters were promised competence and stability. They were promised growth. Taxpayers are entitled to ask a fair question: If this is economic competence, why are we still paying so much to borrow?

Leave a comment